Welcome back to our Spaceballs-inspired exploration of the Canadian Portfolio Manager’s (CPM’s) latest four model portfolios. Our models now range from our simple (but not simplistic!) Light portfolios, to our bordering-on-insanely complicated Plaid portfolios. Today, we’ll introduce our moderately complicated Ridiculous portfolios.

To be honest, most of you can probably begin and end your adventures with a Light portfolio; you’ll still be light years ahead of most DIY investors. But I know some of you may prefer to boldly go where no DIYers have gone before. That’s fine, as long as you’re up for the challenge, and you know all the facts. Most importantly, managing a more complex portfolio is, unsurprisingly, more troublesome. Is it worth it? Usually not. But for the uncommonly intrepid, there may be rewards worth reaping.

After you’ve considered today’s Ridiculous model portfolios, it’s your call: Will you continue onward, or hit the emergency stop button and head toward the Light? You decide; but first, read on.

A Really, Really, Ridiculously Good-Looking Model

The Ridiculous portfolio reports are available for download in the Model ETF Portfolios section of the Canadian Portfolio Manager blog. Clicking on either the Vanguard or iShares ETF buttons in Step 2 will generate the report in a separate tab.

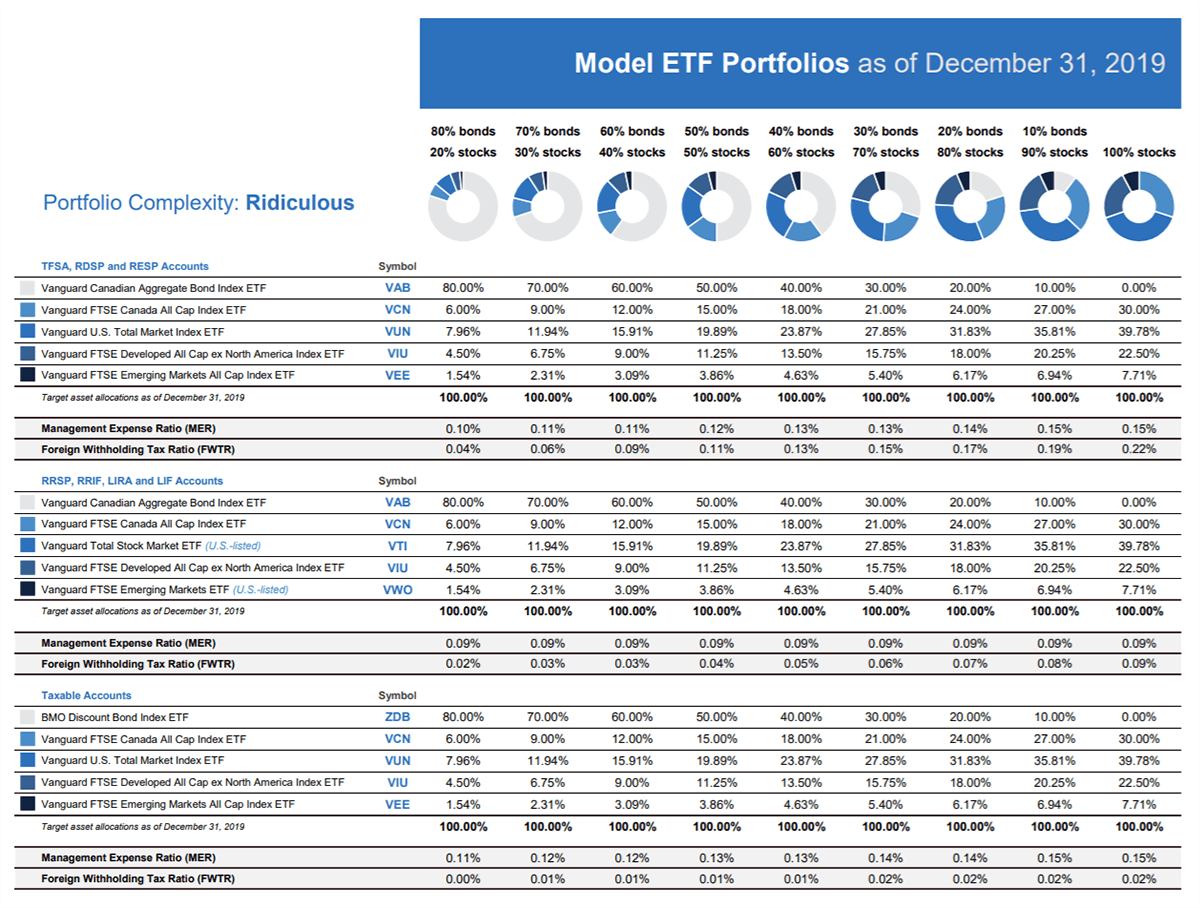

Similar to their Light portfolio counterparts, the Vanguard or iShares Ridiculous portfolios are displayed from left to right, ranging from a very conservative 80% bond, 20% stock portfolio, all the way to a very aggressive 100% stock portfolio. Below the blue and grey donuts, you’ll find the percentage weights allocated to each ETF. To allow for cost comparisons and other portfolio management conveniences, I’ve used the same Canadian, U.S., international, and emerging markets equity ETF weightings in both the Ridiculous and Light portfolios.

The report is further divided horizontally into three account-type sections:

-

- TFSA, RESP, and RDSP Accounts

- RRSP, RRIF, LIRA, and LIF Accounts

- Taxable Accounts

In each section, we’ve adjusted the specific holdings to reduce product costs and increase tax efficiency within the overall portfolio. For each asset mix, you’ll also find the weighted-average management expense ratio (MER), as well as the foreign withholding tax ratio (FWTR).

You can directly compare these figures to those found in the Light portfolio reports. For example, in an RRSP, the Vanguard 40% bond/60% stock Ridiculous portfolio would have a combined MER and FWTR of 0.14%. In comparison, the Vanguard Balanced ETF Portfolio (VBAL) from the Light portfolio report would cost 0.42% in an RRSP, for a total cost difference of 0.28% per year.

Although the report looks intimidating, there are only a handful of differences between the Ridiculous and the Light portfolios. I’ll take you through them now.

Fixed Income Differences: Light vs. Ridiculous

Foreign bonds. I’ve dropped the Vanguard U.S. Aggregate Bond Index ETF (CAD-hedged) (VBU) and the Vanguard Global ex-U.S. Aggregate Bond Index ETF (CAD-hedged) (VBG) from the Vanguard Ridiculous portfolios, due to their higher product costs and foreign withholding taxes. I’ve instead opted for the Vanguard Canadian Aggregate Bond Index ETF (VAB) in all account types except taxable accounts. This change also reduces the holdings in an already-complex portfolio.

As iShares doesn’t yet provide CAD-hedged versions of their U.S.-based bond funds, it was an easy decision to stick with the iShares Core Canadian Universe Bond Index ETF (XBB) in most account types.

Short-term corporate bonds. I’ve also excluded the iShares Core Canadian Short Term Corporate + Maple Bond Index ETF (XSH) from the iShares Ridiculous portfolios. This decision (along with excluding U.S. bonds) increases the duration risk from 7 years for the iShares Light portfolios to 8 years for the iShares Ridiculous portfolios.

Tax-efficient bonds. In taxable accounts, I’ve swapped out VAB and XBB in favour of the BMO Discount Bond Index ETF (ZDB). Because it invests in lower-coupon bonds, with less taxable annual interest, ZDB is expected to be slightly more tax-efficient than the other two.

Equity Differences: Light vs. Ridiculous

U.S.-listed foreign equity ETFs. In tax-deferred accounts (like RRSPs, RRIFs, LIRAs, and LIFs), I’ve replaced the Vanguard U.S. Total Market Index ETF (VUN) with the U.S.-based Vanguard Total Stock Market ETF (VTI). I’ve also replaced the Vanguard FTSE Emerging Markets All Cap Index ETF (VEE) with the U.S.-based Vanguard FTSE Emerging Markets ETF (VWO). These changes reduce product costs and foreign withholding taxes in tax-deferred accounts.

I decided to leave the Vanguard FTSE Developed All Cap ex North America Index ETF (VIU) alone for now. It’s nearly as tax-efficient as other comparable U.S.-based ETFs, and there is no perfect U.S.-based substitute for it. If you’d rather squeeze every last basis point out of your international equity ETFs, I’ve provided some ideas in my blog post, More Alternatives to Vanguard’s Asset Allocation ETFs.

The iShares Light portfolios already hold the U.S.-based iShares Core S&P Total U.S. Stock Market ETF (ITOT) and iShares Core MSCI Emerging Markets ETF (IEMG). But, as asset allocation ETFs with a fund-of-funds wrap structure, these funds don’t benefit from the usual tax advantages. Instead, a Canadian investor can hold ITOT or IEMG directly in their RRSP, and eliminate the 15% U.S. withholding tax on foreign dividends. To reap this tax benefit, I’ve placed these U.S.-based ETFs in the iShares Ridiculous portfolios as direct buys. To further reduce product costs I’ve also swapped out the Canadian-based iShares Core MSCI EAFE IMI Index ETF (XEF) for the U.S.-based iShares Core MSCI EAFE ETF (IEFA). If you’d rather stick with XEF, that’s fine too.

In TFSAs and taxable accounts, I’ve included only Canadian-based iShares foreign equity ETFs. In terms of foreign withholding tax, there is no advantage to using U.S.-based ETFs in these account types, so why bother? In fact, doing so can sometimes lead to even higher withholding taxes.

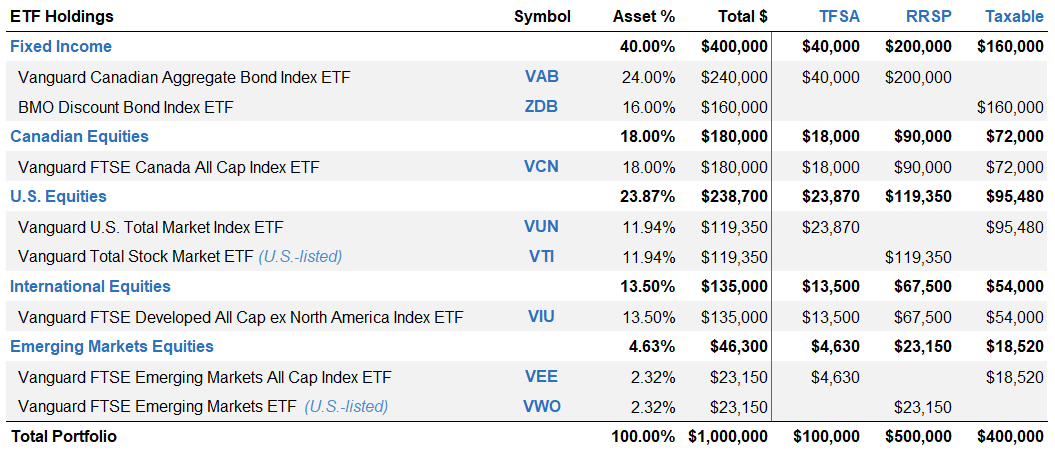

With all these confusing details to track, a Ridiculous example seems appropriate. In the chart below, I’ve illustrated a balanced Vanguard 60% equity, 40% fixed income portfolio worth $1 million, with $100,000 in a TFSA, $500,000 in an RRSP, and $400,000 in a taxable account.

Example: Ridiculous Balanced ETF Portfolio

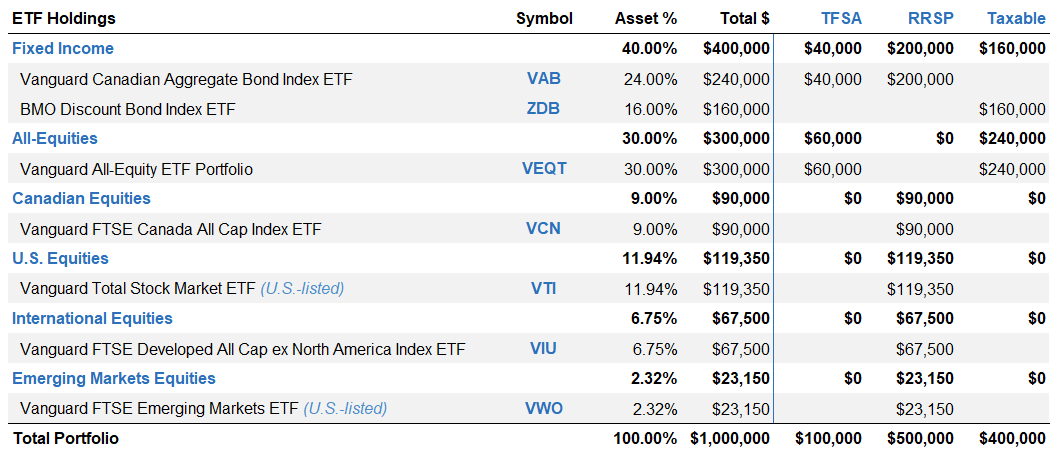

Using VEQT and XEQT in TFSA and Taxable Accounts

If you’re overwhelmed by the number of holdings above, we may be able to tone it down for you. Instead of holding four equity ETFs in your TFSA or taxable accounts, you could swap your VCN/VUN/VIU/VEE holdings for the Vanguard All-Equity ETF Portfolio (VEQT), or your XIC/XUU/XEF/XEC holdings for the iShares Core Equity ETF Portfolio (XEQT). The Ridiculous portfolios’ equity region weights are identical to the 100% Vanguard and iShares asset allocation ETFs, so you can think of them as interchangeable. Your product costs will increase slightly, but you’ll still maintain most of your cost savings, with slightly less ridiculous portfolio management.

Example: (Slightly Less) Ridiculous Balanced ETF Portfolio

Advantages of the Ridiculous Portfolios

Now that you’re familiar with the Ridiculous portfolios, let’s discuss some of their potential benefits.

Lower product costs. By ditching some of the higher-cost foreign bond ETFs, adding a dose of lower-cost U.S.-based foreign equity ETFs, and performing your own portfolio rebalancing, you can further reduce your already rock-bottom product costs.

Lower foreign withholding taxes. By opting for U.S.-listed foreign equity ETFs in your RRSP, you can reduce the unrecoverable withholding taxes on your foreign dividends.

Lower income taxes. Holding lower-coupon bond ETFs like ZDB in your taxable accounts can increase your after-tax return – at least relative to holding traditional bond ETFs, like VAB or XBB. It’s coupon clipping at its finest.

Increased ability to customize. What if you don’t like the equity weights or specific ETF holdings in the Ridiculous portfolios? No problem. You can mix and match them to your liking.

More tax-loss selling opportunities in your taxable account. If you’re investing in multiple ETFs in a taxable account, one or more of them may be in the red more often than a one-fund balanced ETF portfolio. A disciplined tax-loss selling strategy could come in handy, especially if you’ve just realized big gains by switching to a new portfolio.

Disadvantages of the Ridiculous Portfolios

By seeking to improve on the Light portfolios, we’re bound to add some relative downsides as well.

You need big accounts. If your RRSP is worth $10,000, you’re only saving about $28 per year on your Ridiculous portfolio, relative to a Light portfolio. And that’s before factoring in your additional trading commissions and currency conversion costs. Make sure your portfolio value is well into 6 digits or higher before considering a switch.

You’ll be placing more trades. More ETF holdings to manage across each account creates more trading costs and complexities. If you’re regularly contributing to your portfolio, the commissions can start to offset some or even all of your cost savings.

You need to rebalance your portfolio. In place of an elegant one-fund solution, your accounts now resemble a crudely constructed Frankenstein’s monster. Good luck manually keeping this beast in balance over time.

You’ll need to track more adjusted cost bases (ACBs) in your taxable account. With more ETFs at play, you’ve got more ACBs to track. Tracking the book value for a single ETF is a whole lot easier.

You’ll need U.S. dollars. To cheaply convert your Canadian dollars to U.S. dollars in your RRSP, you’ll need to master Norbert’s gambit. As described in my bonus section below, this strategy has a cost, so you’ll also need to ensure you’re only converting larger amounts. I’d say at least $10,000 a pop.

A Ridiculous Waste of Time?

Are you ready to replace your nearly perfect asset allocation ETF for a slightly cheaper Ridiculous portfolio? Before you go, know that I’m not a big fan of them in their current form. I don’t even typically manage my client portfolios like this. That’s right, just like Dark Helmet in Spaceballs, I too prefer to skip over Ridiculous and head straight to Ludicrous with my portfolio complexity.

So why bother with the Ridiculous portfolios in the first place? Great question. As we continue on our quest for portfolio perfection, we’ll be using the same ETFs from the Ridiculous portfolios, but adjusting their weights in each account type to maximize overall tax efficiency.

Bonus: Estimating the Cost of Norbert’s Gambit

As I mentioned earlier, if you plan to use the Norbert’s gambit strategy to convert Canadian dollars (CAD) to U.S. dollars (USD) in your RRSP, $10,000 would be a good minimum starting point per transaction. But how much does each conversion really cost? Good news: I’ve got a process for figuring that out.

For our example, we’ll assume you want to convert $10,000 CAD to USD, and buying and selling DLR and DLR.U costs $9.95 per trade. Adjust accordingly if your commissions are different, or you also are subject to Electronic Communication Network (ECN) fees.

Step 1: Calculate the U.S. dollars you’d receive based on the current spot rate.

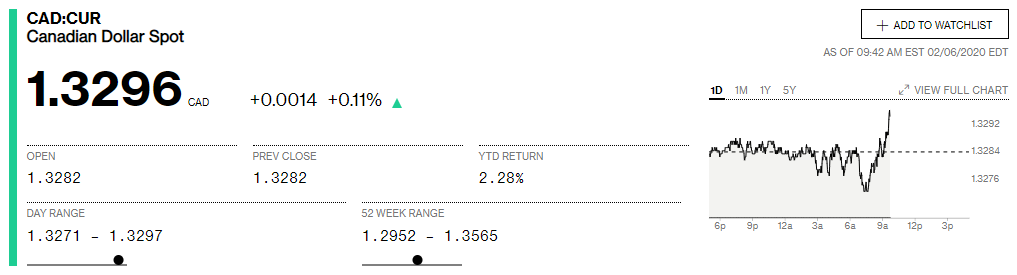

We first need to determine a fair conversion price, so we can compare it to our Norbert’s gambit outcome. For this, we need to know the spot (or benchmark) rate for converting CAD to USD. Bloomberg publishes a Canadian dollar spot rate we can use. Simply divide the CAD amount you’d like to convert by the quoted spot rate on their website. In our example, dividing $10,000 CAD by 1.3296 CAD/USD gives us $7,521.06 USD.

Source: Bloomberg, as of February 6, 2020 (9:45 am ET)

Step 2: Determine the current ask price for DLR and bid price for DLR.U.

When we obtained the spot rate from Bloomberg, DLR had a current per-share ask price of $13.45 CAD; DLR.U had a current per-share bid price of $10.11 USD.

| Security |

Symbol |

Bid |

Ask |

| Horizons U.S. Dollar Currency ETF |

DLR |

$13.44 |

$13.45 |

| Horizons U.S. Dollar Currency ETF |

DLR.U |

$10.11 |

$10.12 |

Source: Quotestream, as of February 6, 2020 (9:45 am ET)

Step 3: Calculate the U.S. dollars you’d receive from the Norbert’s gambit.

- Subtract trading commissions (and ECN fees) from your Canadian dollars. This will provide you with your net CAD after trading costs:

$10,000 CAD – $9.95 CAD = $9,990.05 CAD

- Divide this figure by the DLR ask price. This will provide you with the number of DLR shares you can purchase with your Canadian dollars. Don’t worry about using partial shares for the calculation; just remember that you can only purchase whole shares when placing your trades:

$9,990.05 CAD ÷ $13.45 CAD = 742.75464684 shares

- Multiply this figure by the DLR.U bid price. This will provide you with your gambit’s U.S. dollar proceeds, before trading commissions:

742.75464684 shares × $10.11 USD = $7,509.25 USD

- Subtract your trading commissions (and ECN fees) from your U.S. dollars. This will provide you with your net U.S. dollars, after trading costs:

$7,509.25 USD – $9.95 USD = $7,499.30 USD

Step 4: Compare the USD proceeds from Step 3 with the USD proceeds from Step 1.

- Subtract the USD calculated in Step 3 from the USD calculated in Step 1. This will provide you with the Norbert’s gambit strategy’s estimated dollar cost in U.S. dollars:

$7,521.06 USD – $7,499.30 USD = $21.76 USD

- Multiply this figure by the spot rate from Step 1. This will put your U.S. dollar cost into Canadian dollar terms:

$21.76 USD × 1.3296 CAD/USD = $28.93 CAD

- Divide this figure by your initial $10,000 CAD conversion amount. This will provide you with the estimated percentage cost of the Norbert’s gambit strategy.

$28.93 CAD ÷ $10,000 CAD = 0.29%

Norbert’s Gambit Results

In this example, the total cost of Norbert’s gambit relative to our benchmark spot rate conversion was around 0.29%. It would take roughly a year for your product cost and foreign withholding tax savings to offset this initial currency conversion cost. That’s not too bad. If your cost exceeds 0.3%, you might want to stick with Canadian-based ETFs instead.

If you’d like to see some gambits in action, feel free to check out my YouTube video tutorials for various brokerages.

A Ludicrously Long Wait

Again, our Ridiculous model portfolios are a bit of a gambit themselves. You might think of them as a stepping stone toward creating even more complex model portfolios. Next up, we’ll take you on a tour through our Ludicrous portfolios, which may arguably be more worth your while.