I received this question from a reader of the blog (it’s also a question I receive on the daily from DIY investors):

“The Vanguard AA ETFs are very appealing in their simplicity in regards to maintenance and range of options. However, I am mindful of the tax-efficiency issues regarding holding these in a taxable account due to the premium bond holdings. Would holding VBAL in a taxable account for the sake of ultimate management ease be “significantly” outweighed by the financial benefit of crafting a more tax-efficient DIY bundle of ETFs in just the taxable account (such as a combo of ZDB, VCN and XAW)?”

As the reader correctly notes, the tax-inefficiencies in Vanguard’s AA ETFs mainly lie with the underlying bonds (not with the equities) – at least in taxable accounts. You see, many of the bonds in fixed income ETFs are currently trading at what’s called a “premium” to their maturity value. This basically means you’ll overpay for the bonds when you purchase them (and get stuck with a capital loss when they mature at a lower value), but receive more interest along the way (this extra interest is meant to compensate you for the initial sticker shock). Problem is, interest is fully taxable as income, whereas the capital loss you realize on the bonds at maturity can only offset capital gains (where only 50% of the gain is taxable). This inconsistent taxation between capital gains and interest income can lead to some interesting after-tax results.

In the following analysis, we’re going to compare the actual before and after-tax returns of a relatively tax-efficient bond fund, the BMO Discount Bond Index ETF (ZDB) with the collection of Vanguard bond ETFs found in Vanguard’s asset allocation funds (with similar weightings):

Each investment will start with $100,000 on January 1, 2015. Taxes on income will be paid when received (at the top Ontario tax rate) and any capital gains will be payable on December 31, 2018 (we have also assumed that any capital losses realized at that time can be used to offset existing capital gains). We’ll look at the before-tax returns first, then the after-tax returns, then throw some GICs into the mix for fun.

First Among Equals

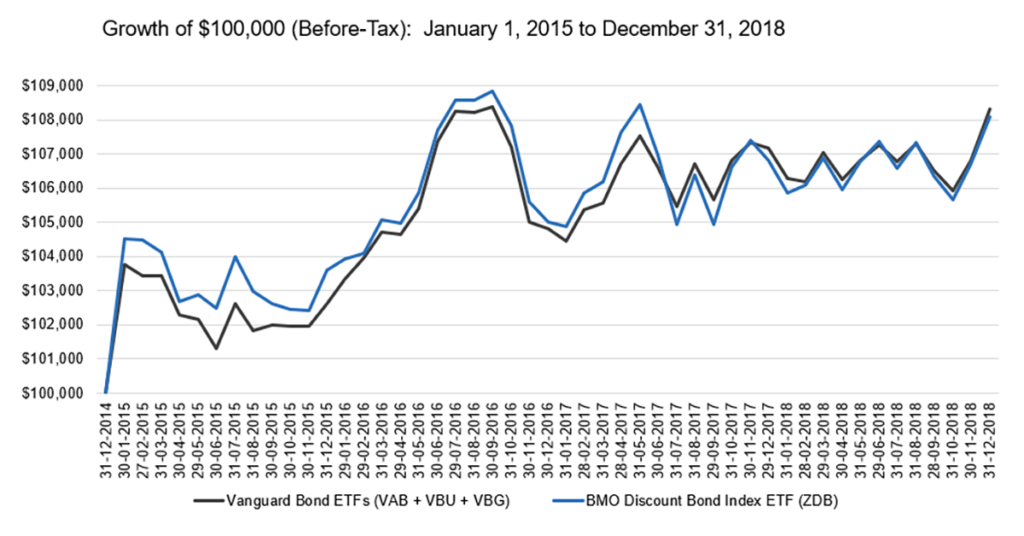

Between 2015 and 2018, the $100,000 position in ZDB grew to $108,075, while the Vanguard bond ETFs grew to a similar value of $108,301. In percentage terms, ZDB returned 1.96% each year on average, while the Vanguard bond ETFs returned 2.01%. As the before-tax returns were nearly identical between the two investment options over the measurement period, this will make for an interesting after-tax comparison next.

Sources: BMO Global Asset Management, Vanguard Investments Canada Inc., cds.ca, taxtips.ca

Tax Me If You Can

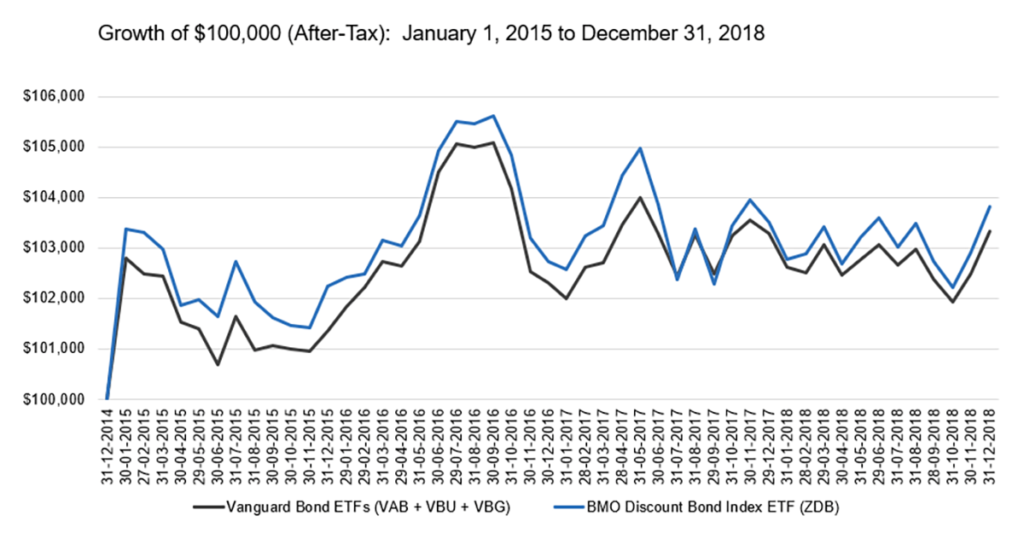

From an after-tax perspective (assuming the top rate for an Ontario taxpayer), the $100,000 position in ZDB grew to $103,821, while the Vanguard bond ETFs grew to only $103,333. In after-tax percentage terms, ZDB returned 0.94% each year on average, while the Vanguard bond ETFs returned 0.82% (for total after-tax outperformance of 0.12% per year).

Sources: BMO Global Asset Management, Vanguard Investments Canada Inc., cds.ca, taxtips.ca

Although 0.12% may seem trivial in the whole scheme of things (and it just might be), the Vanguard bond ETFs would have needed to earn an additional 0.25% per year before-tax if they had a chance of eking out another 0.12% per year after-tax [0.25% × (1 – 53.53% top Ontario tax rate)]. So, if 0.25% is the ballpark tax drag from these less efficient Vanguard bond ETFs, what does this translate into for taxable investors of the Vanguard asset allocation ETFs?

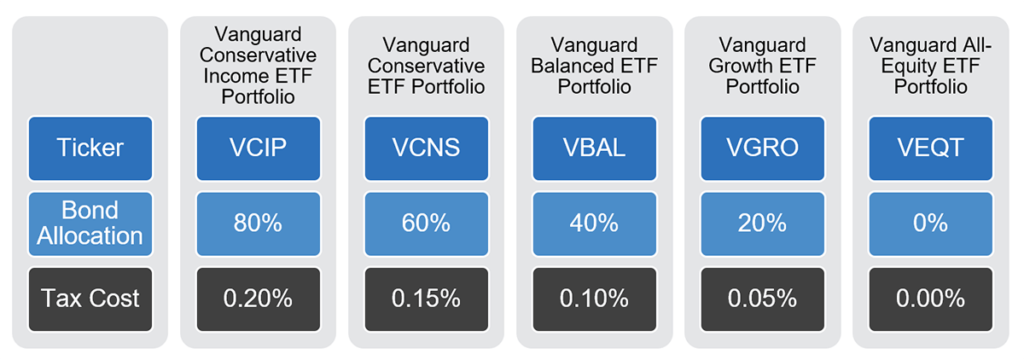

That depends on which ETF you’re invested in, as only the bond component has the potential for this specific “premium bond” tax cost. The more conservative your asset allocation, the greater the expected tax drag. For example, the estimated tax cost for the Vanguard Growth ETF Portfolio (VGRO), which allocates 20% to bonds, is only 0.05% (20% bond allocation × 0.25% tax cost), while the Vanguard Balanced ETF Portfolio (VBAL), which has a 40% allocation to bonds, is 0.10% (40% bond allocation × 0.25% tax cost). I’ve included a summary of the estimated additional tax cost for each Vanguard ETF in the image below.

Estimated Premium Bond Tax Cost in a Taxable Account

Sources: BMO Global Asset Management, Vanguard Investments Canada Inc., cds.ca, taxtips.ca

So, should you avoid these ETFs in taxable accounts entirely? I don’t think so, especially if they help you maintain discipline and stay invested. Managing more than one ETF requires slightly more effort, and trying to keep up to speed on all the tax jargon is exhausting (take my word for it). Potentially giving up 10 basis points of return for less time with family and friends doesn’t seem worth it to me, but I’ll let you decide for yourself. I’ve also outlined another fixed income alternative below.

Climbing the GIC ladder

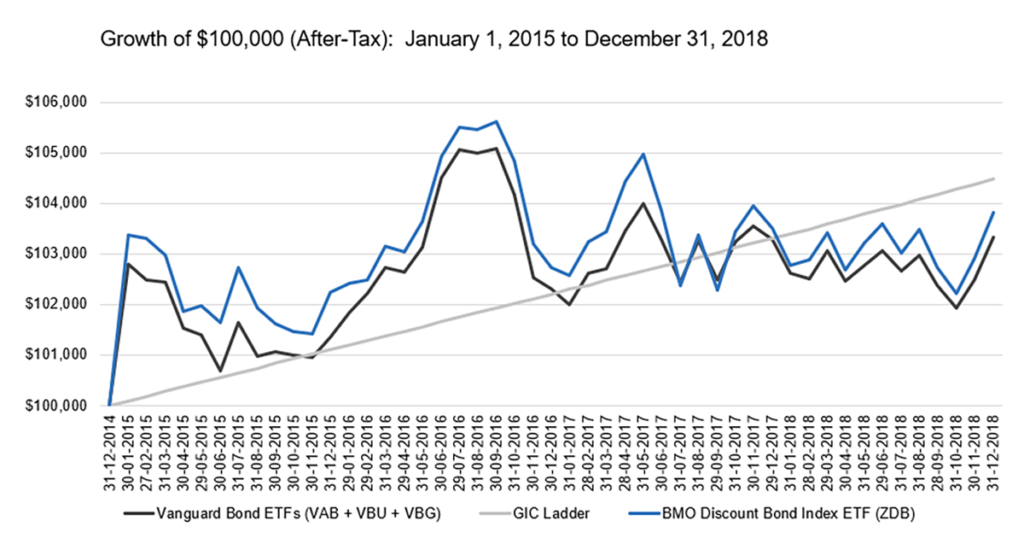

If the exhilarating highs and depressing lows of fluctuating bond prices get you down, there is another option. A GIC ladder could be a suitable alternative to short-term or even broad-market bond ETFs (like ZDB or the Vanguard bond ETFs). This is especially true when the yield-to-maturity (YTM) of the GIC ladder is higher than that of the bond ETFs, like it is now.

After back-testing this strategy over the same measurement period, we found the GIC ladder climbed to $104,473 (light grey line in the graph below), or 1.10% per year on average after-tax (with a much smoother ride than the bond ETFs). You could even consider combining GICs and ZDB in your taxable account, to ensure you have enough liquidity for rebalancing your portfolio. For more information on this strategy, please read: The Most Boring Battle Ever: Bond ETFs or GICs?

Sources: BMO Global Asset Management, NBIN, Vanguard Investments Canada Inc., cds.ca, taxtips.ca