In my previous blog post, I talked about Environmental, Social and Governance (ESG) investing, why investors are interested and the different ways to implement it in your portfolio. This naturally raises the next question: how rigorous is the ESG research and does it actually differentiate and reward good from bad behavior?

The natural fear is that ESG investing is simply ‘green washing,’ the investing equivalent of ‘white washing’ your house before you sell it. Cover up those pesky cracks and hope buyers won’t notice… Green washing is when a company spends more time and money on marketing and advertising than on business practices that minimize environmental, social or governance issues. So how can you know if a company is actually behaving well?

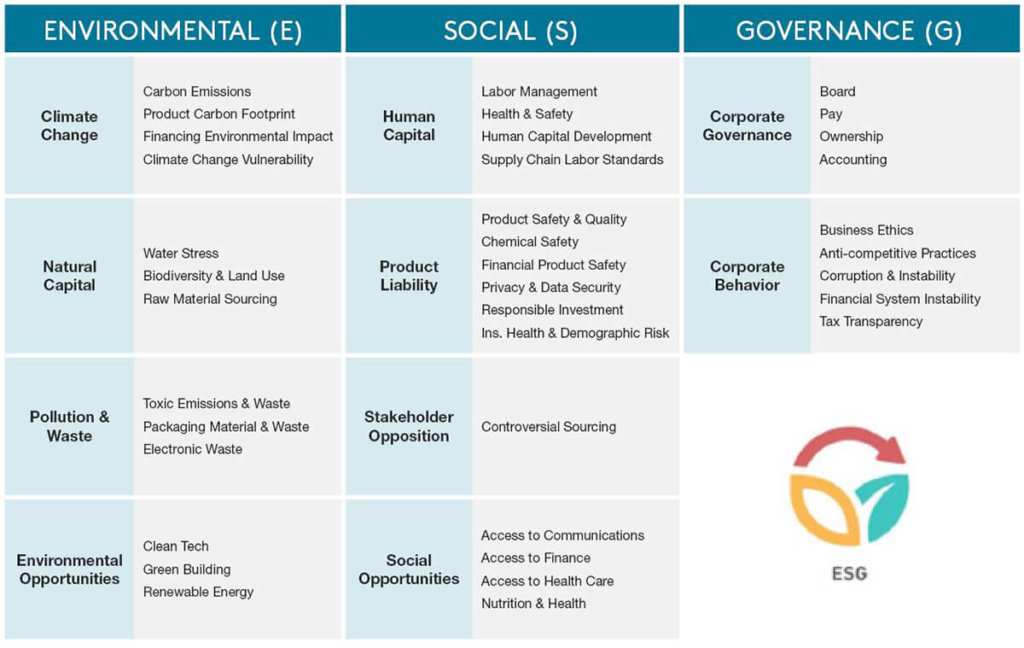

The growing interest in Socially Responsible Investing (SRI) has led to the development of ESG rating agencies, who have developed and use wide-ranging and rigorous criteria to evaluate companies and industries. For each company and industry, a sub-set of criteria are designated as Key Performance Indicators (KPIs). For example, a company like Microsoft need not be concerned about toxic waste, but should pay a lot of attention to data privacy and board governance issues. Companies in the oil & gas industry won’t be concerned about data privacy, but should be very concerned about their carbon emissions.

Each rating agency defines their own criteria and KPI but they all generally follow these guidelines:

Chart 1: Key Performance Indicators

Based on these criteria, an ESG investment strategy will re-weight, exclude, or include companies in the portfolio depending on how they score at the company and industry level. I wrote about these investment strategies in my previous blog: What is Socially Responsible Investing?

Having read all 95 pages of MSCI’s ESG report on Microsoft, I can confirm that these ratings look deep into the company on a wide range of issues that are all very pertinent to investor decision making.

One of the concerns with ESG investing is the lack of standardization in the measurement of these criteria. The Sustainability Accounting Standards Board (SASB) was established in 2011 with the specific goal of encouraging ESG disclosure among public companies. These standards are making it easier and more efficient for companies to report material issues to stakeholders. At the same time, they are improving comparability of the metrics for investors.

While the standards are still far from mainstream, they are rapidly improving and increasingly being adopted by public companies. As more investors demand accountability on ESG issues, companies have to answer.

In my final blog post in this series, I’ll look at how ESG investing affects investment performance.