I recently received a great question from a reader, and I promised him I would follow up with a detailed blog post. Here it is!

David: Justin, I was wondering if you have any explanations as to why VBU and BND have significant differences in returns over the past few calendar years, even though they hold the same U.S. bonds?

Performance of VBU vs. BND: 2016–2018

| Security |

Symbol |

2018 |

2017 |

2016 |

| Vanguard U.S. Aggregate Bond Index ETF (CAD-hedged) |

VBU |

–1.02% |

2.86% |

2.15% |

| Vanguard Total Bond Market ETF |

BND |

–0.04% |

3.62% |

2.57% |

| Actual underperformance of VBU |

|

–0.98% |

–0.76% |

–0.42% |

Sources: The Vanguard Group Inc., Vanguard Investments Canada Inc.

Bender: I hear you, David. The Canadian-listed Vanguard U.S. Aggregate Bond Index ETF (CAD-hedged) (VBU) simply holds the U.S.-listed Vanguard Total Bond Market ETF (BND), and hedges away the fund’s U.S. currency exposure. So, a Canadian VBU investor might expect to earn roughly the same return as BND, at least after subtracting VBU’s additional product fees and foreign withholding taxes.

The problem is, these additional costs still don’t fully explain VBU’s underperformance. You also have to factor in the returns from VBU’s currency-hedging strategy (also known as the fund’s hedge return).

A Home Bond Advantage?

Vanguard Canada hedges the U.S. currency exposure in VBU by striking a deal with a counterparty (such as a bank). This allows Vanguard to convert their U.S. dollars back to Canadian dollars at a predetermined rate and time (usually between 1–3 months). This strategy offsets most of the U.S. dollar exposure for Canadian VBU investors.

The pricing of the future (or “forward”) exchange rates is largely based off interest rate differentials between the two countries. In this case, that’s between Canada and the U.S.:

- If the foreign country (U.S.) has higher interest rates than the domestic country (Canada), this can generate a negative hedge return for the Canadian investor.

- If the foreign country (U.S.) has lower interest rates, this can generate a positive hedge return for the Canadian investor.

This forward pricing mechanism ensures you can’t earn a risk-free return by investing in a higher-yielding foreign bond with a similar risk profile as your home country’s bonds.

Currency-Hedge Hog

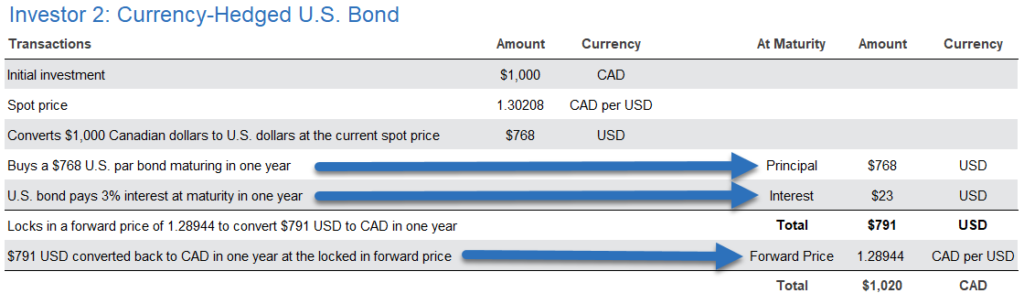

An example might help. Suppose interest rates in Canada are 2%, while U.S. investors currently enjoy 3%. Two Canadians each have $1,000 CAD to invest in a one-year bond.

Investor 1 buys a Canadian par bond maturing in one year and paying 2% interest at that time (or $20 CAD). After a year, Investor 1 receives their original $1,000 back, plus $20 of interest, for a total of $1,020 CAD.

Investor 2 believes they see an arbitrage opportunity, and instead converts their $1,000 CAD into $768 USD, at a spot price of 1.30208. They then purchase a $768 U.S. par bond, maturing in one year and yielding 3%. That’s about $23 USD ($768 × 3%). After patting themselves on the back for earning an extra 1% of risk-free return, they realize they’ve totally forgotten about their U.S. dollar currency risk.

To offset their U.S. dollar exposure, they immediately enter into a one-year forward contract where a counterparty agrees to exchange $791 U.S. dollars ($768 principal + $23 interest) for Canadian dollars when the bond matures in a year, at a forward price of 1.28944.

After crunching the numbers ($791 USD × 1.28944 = $1,020 CAD), Investor 2 realizes they’re no better off than if they had simply invested $1,000 CAD in a one-year Canadian bond yielding 2%. Although they receive 3% interest on the U.S. bond, they lose 1% (or $10) of interest when they convert their U.S. dollars back to Canadian dollars at a lower one-year forward rate. This $10 loss is their “return” from the currency-hedging strategy.

The View from Canada

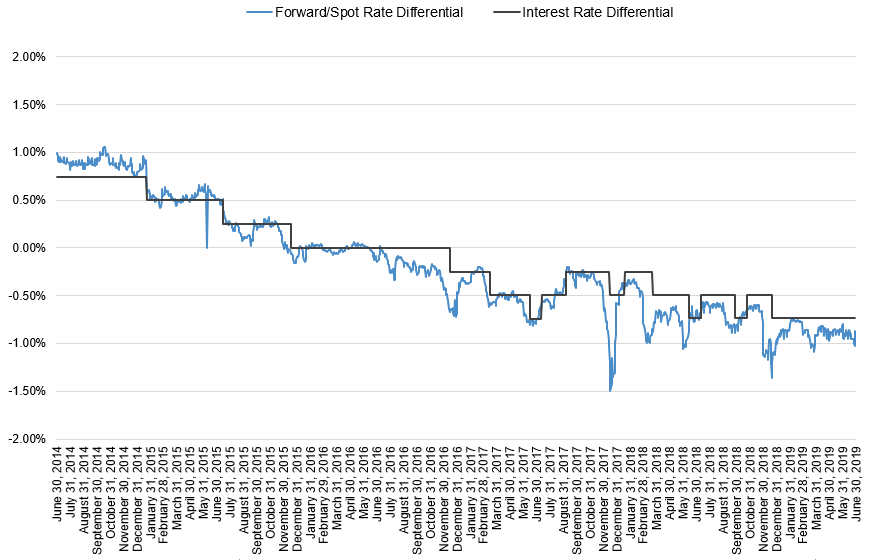

Hedge returns can fluctuate over time, as the interest rate differentials change between countries. Consider the one-month forward rates/spot rates for the Canadian vs. U.S. dollar since VBU’s inception. The average hedge return was positive in the first couple years (the blue line in the graph below). It has since turned negative over the last few years, as interest rate differentials between Canada and the U.S. have reversed course (the dark grey line in the graph below).

In 2016, 2017, and 2018, average hedge returns were –0.33%, –0.76%, and –1.03%, respectively. This was to be expected, as U.S. interest rates were higher than Canadian interest rates over the past three calendar years.

Thus, a Canadian investor buying currency-hedged U.S. bonds over the past three years should have expected an additional return drag relative to a U.S. investor buying those same bonds.

U.S. Dollar Hedging “Return” from a Canadian Perspective

Historical forward/spot rate differentials are estimated by dividing the one-month forward rate of USD (CAD per USD) by the spot rate of USD (CAD per USD), and subtracting one. Historical interest rate differentials are estimated by dividing one plus the federal funds target rate (Federal Reserve) by one plus the target for the overnight rate (Bank of Canada), and subtracting one.

Sources: Bloomberg, Bank of Canada, Federal Reserve

Returning to VBU’s Currency-Hedging Strategy

Let’s compare the actual underperformance of VBU to its expected underperformance each year. (Expected underperformance is VBU’s foreign withholding taxes + additional product fees + average annual currency-hedging costs.) We find they have been very similar.

Performance of VBU vs. BND: 2016–2018

| Security |

2018 |

2017 |

2016 |

| Vanguard U.S. Aggregate Bond Index ETF (CAD-hedged) (VBU) |

-1.02% |

2.86% |

2.15% |

| Vanguard Total Bond Market ETF (BND) |

-0.04% |

3.62% |

2.57% |

| Actual underperformance of VBU vs. BND |

-0.98% |

-0.76% |

-0.42% |

Sources: The Vanguard Group Inc., Vanguard Investments Canada Inc., Bloomberg, Bank of Canada, Federal Reserve

Expected underperformance of VBU vs. BND: 2016–2018

| Fund expenses |

2018 |

2017 |

2016 |

| Foreign withholding taxes |

-0.13% |

-0.09% |

-0.02% |

| Additional product fees |

-0.19% |

-0.17% |

-0.17% |

| Average cost from currency-hedging |

-0.71% |

-0.50% |

-0.14% |

| Expected underperformance of VBU vs. BND |

-1.03% |

-0.76% |

-0.33% |

Sources: The Vanguard Group Inc., Vanguard Investments Canada Inc., Bloomberg, Bank of Canada, Federal Reserve

Hedging Expectations

So, what returns can we expect from currency-hedged global bond ETFs going forward? In my next post, we’ll estimate the hedge ratios of the Vanguard U.S. Aggregate Bond Index ETF (CAD-hedged) (VBU) and the Vanguard Global ex-U.S. Aggregate Bond Index ETF (CAD-hedged) (VBG), both of which are included in the Vanguard Asset Allocation ETFs.