“It’s not you, it’s me”.

These words have been professed during breakups throughout history, so we all know what they really mean:

“I can do better”.

And maybe you can. True, your life has been simpler and more balanced since you paired up last year, but the thrill is gone. Plus, you’d love to find someone less demanding on your wallet. Sure, a new relationship may complicate your life in other ways, but your mind is made up: You’ve decided it’s time to sell your Vanguard Asset Allocation ETF.

Before you do, let’s look at some of the pros and cons.

Separation Anxiety

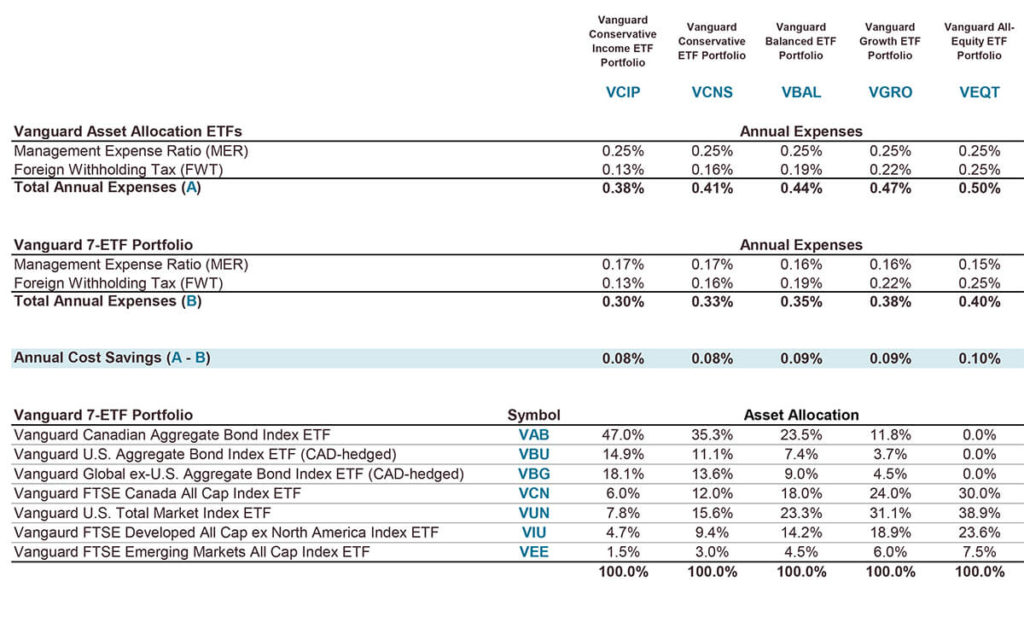

One of the many benefits of the Vanguard Asset Allocation ETFs is convenience. You need only place a single trade to gain exposure to a basket of Vanguard’s globally diversified ETFs. You also avoid the hassle of having to manually rebalance your ETF portfolio each time you add new money to your accounts.

For this automatic rebalancing feature, Vanguard charges a very reasonable 0.08%–0.10% per year on top of the underlying 0.15%–0.17% annual ETF fee. To put this in perspective, if your portfolio is worth $100,000, you pay Vanguard another $80–$100 per year for automatic rebalancing. Most robo-advisors charge 4–5 times that for similar service (although to be fair, the Vanguard option still requires you to place some trades).

In the chart below, I’ve compared the annual cost savings from breaking up a Vanguard asset allocation ETF into its underlying holdings. You’ll notice the savings are the result of a slightly reduced MER; the foreign withholding taxes are the same either way.

If these modest savings don’t get you excited, I can’t really blame you. However, if you have substantial RRSP assets, there are more portfolio tweaks you can make to reduce your annual costs by up to 0.37%. That may be enough money to help you get over the heartache of a break-up.

Sources: Vanguard Investments Canada Inc., The Vanguard Group, Inc., Bloomberg, FTSE Russell, CRSP, as of December 31, 2018

Sources: Vanguard Investments Canada Inc., The Vanguard Group, Inc., Bloomberg, FTSE Russell, CRSP, as of December 31, 2018

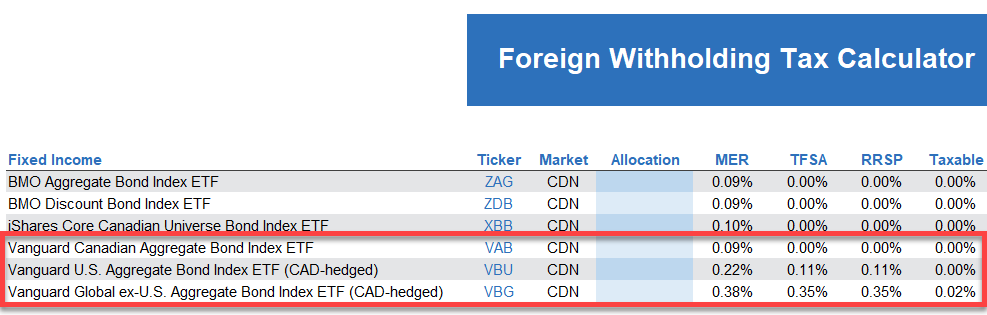

Ditch Foreign Bonds

With annual bond yields hovering around 2% these days, you can’t afford to be frivolous with your fixed income investments. If you’re already planning to buy the underlying Vanguard ETFs directly, you could take this opportunity to forgo the foreign bond ETFs, which have higher costs and foreign withholding taxes than comparable Canadian bond ETFs. The trade-off is that your portfolio’s fixed income investments will no longer be globally diversified.

Sources: Vanguard Investments Canada Inc., The Vanguard Group, Inc., Bloomberg, as of December 31, 2018

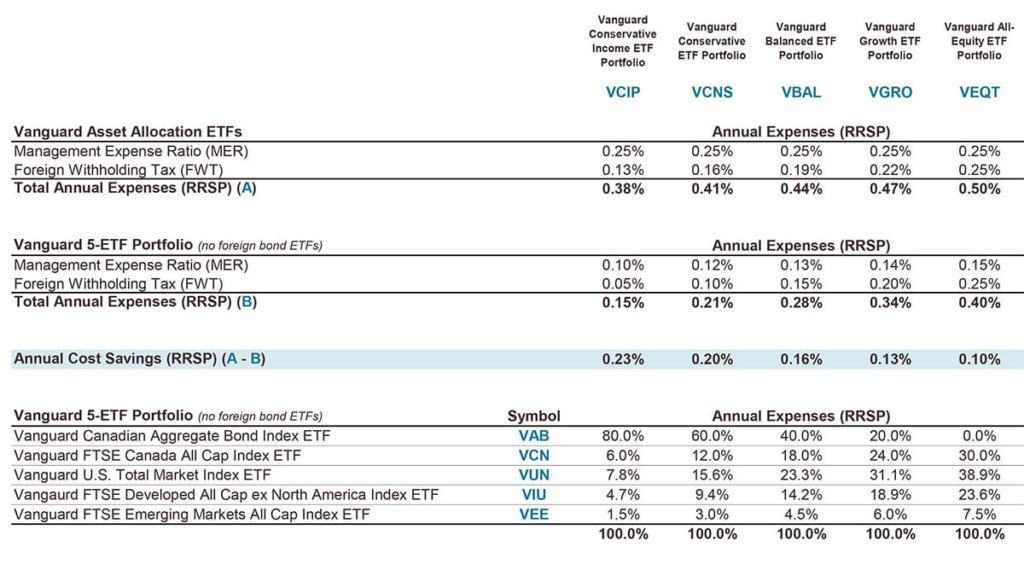

By excluding the two foreign bond ETFs, your 7-ETF portfolio decreases to 5, reducing the number of moving parts you must tend to. Plus, you could increase your annual RRSP cost savings by between 0.10%–0.23%.

Sources: Vanguard Investments Canada Inc., The Vanguard Group, Inc., FTSE Russell, CRSP, as of December 31, 2018

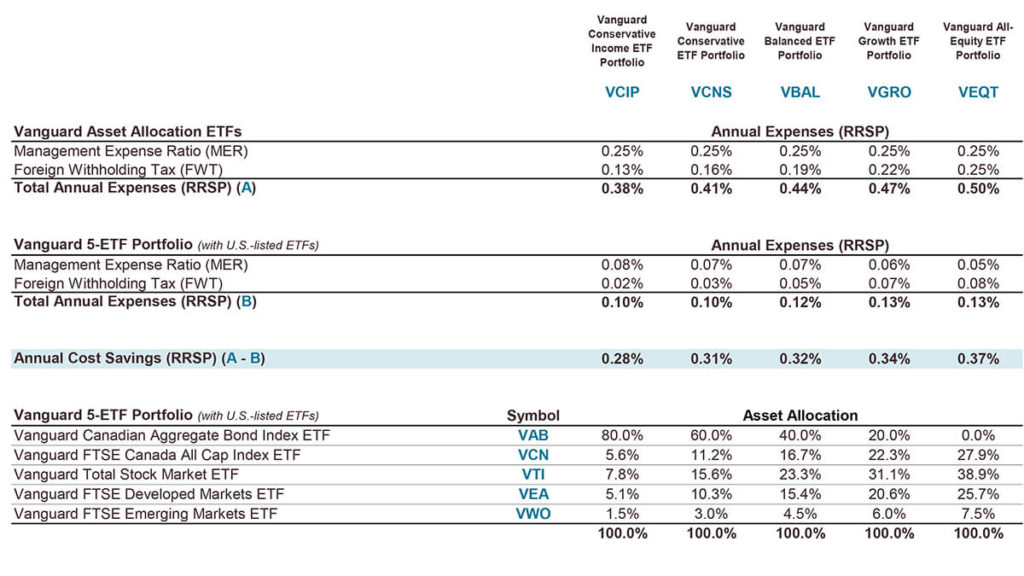

Buy American

Finally, if you’re investing within an RRSP, there’s even more opportunity to reduce your costs by switching to U.S.-listed foreign equity ETFs. Not only are they cheaper than their Canadian-listed counterparts, they’re also more tax-efficient in an RRSP. This can substantially reduce the drag from foreign withholding taxes.

It Can All Add Up

If you’ve been following along, your total annual cost savings from all these changes can range between 0.28%–0.37%. That’s a savings you could learn to love.

In the 5-ETF portfolio below, the Vanguard U.S. Total Market Index ETF (VUN) has been swapped with the Vanguard Total Stock Market ETF (VTI), while the has been replaced with the Vanguard FTSE Emerging Markets ETF (VWO).

You could continue to hold the Vanguard FTSE Developed All Cap ex North America Index ETF (VIU). But swapping it for the Vanguard FTSE Developed Markets ETF (VEA) can further maximize your savings.

That said, there’s extra work involved if you do. Unlike VIU, VEA invests over 8% of the fund in Canadian companies. So, you’d want to adjust your allocation to VEA to avoid short-changing yourself on international stocks. This adjustment also increases your portfolio’s weight to Canadian equities, so you’d reduce your allocation to the Vanguard FTSE Canada All Cap Index ETF (VCN) accordingly.

Sources: Vanguard Investments Canada Inc., The Vanguard Group, Inc., FTSE Russell, CRSP, as of December 31, 2018

The Grass Is Not Always Greener

For me, the cost savings become most enticing after the final step of including U.S.-listed ETFs. But before you decide to make a clean break of it, make sure the following applies to you:

You have significant RRSP investments. If your RRSP is worth $10,000, you’re only saving up to $37 per year (before costs), but adding a lot of financial chores to your day. IMO, that’s totally not worth it.

Your brokerage doesn’t charge trading commissions on ETF purchases. If you’re paying $10 for each ETF trade, the trading costs can soon easily offset the savings. If you’re going to make the switch to individual ETFs, consider switching to a low-cost brokerage too.

You’re comfortable performing Norbert’s gambit at your brokerage. To purchase U.S.-listed ETFs, you’ll need to cheaply and efficiently convert your Canadian dollars to U.S. dollars. The Norbert’s gambit strategy is your best bet in this regard, so you’d better be a pro at it.

You enjoy working with portfolio rebalancing calculators. Remember, any time you add new money to your accounts, you’ll need to visit Vanguard’s site, collect the underlying ETF target weights for your desired asset allocation ETF, input them into your calculator, and place multiple trades. Your one-minute biweekly task has now stretched into at least a half-hour.

You’re good with numbers. You’ll also need to take the Canadian dollar figures from your rebalancing spreadsheet and convert them into U.S. dollars before calculating how many shares of each U.S.-listed ETF to purchase. If you tend to mix up whether to multiply or divide a quoted currency pair, you and your portfolio could be in for a world of pain.