This blog post is adapted from my French column with the newspaper Les Affaires

My esteemed colleague Yves Rebetez recently wrote a very interesting article1 about the merits of using ETFs to manage currency risk in your portfolio. I would like to add a few points that I think deserve your attention.

If you have adopted a modern portfolio strategy, you most likely hold both Canadian and foreign investments in order to improve diversification. When the Canadian dollar appreciates, your return on foreign investments generally depreciates, and vice versa. The ETF market offers tools for accepting or hedging currency risk. Many foreign stock ETFs are available in both hedged and unhedged versions. To help you choose, here are a few tips and observations.

1. Foreign bonds should always be hedged!

Bonds help stabilize your portfolio. But when you accept the currency risk of your foreign bond investments, you greatly increase the volatility of your portfolio. Hedging currency risk is also cost-effective for bonds. So, for goodness’ sake, hedge them! The exception to this rule is if you regularly have major expenses in a foreign currency. For example, a snowbird will have unhedged bonds in US dollars.

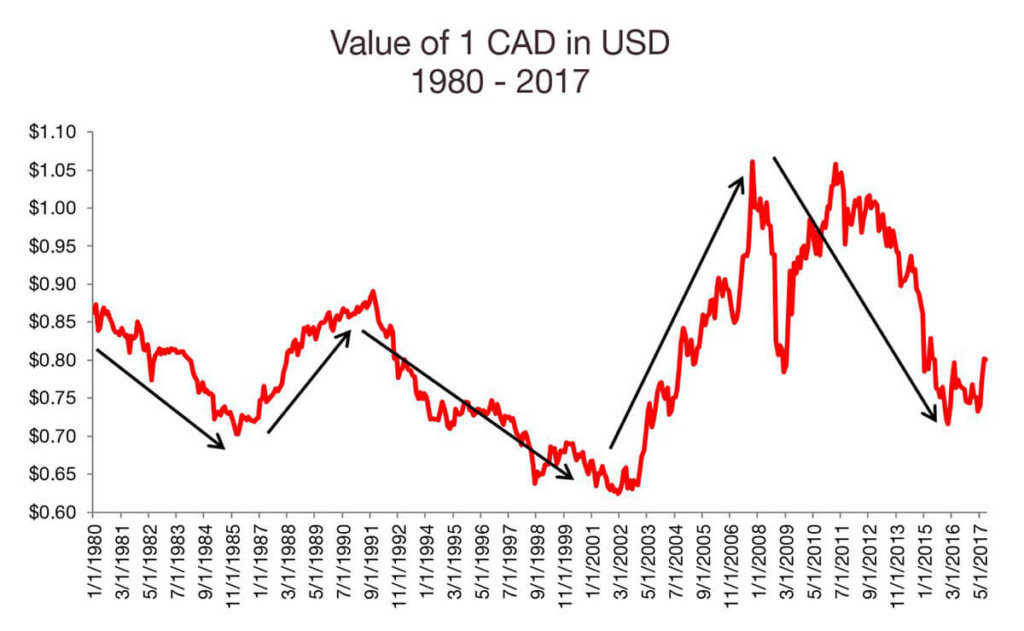

2. The Canadian dollar tends to appreciate and depreciate in cycles

Unlike bonds, stocks handle currency risk fairly well. For example, in the past five years, the S&P 500 index has reported similar volatility in both Canadian (11.4%) and American (10.9%) dollars. Therefore, if the gains and losses related to currencies tended to offset each other year over year, we would not need to worry about hedging this risk. Alas! The Canadian dollar often appreciates and depreciates in cycles of several years, as shown in the graph below. If you do not hedge the currency risk, and the Canadian dollar starts to boom, it will take you years to recover the foreign currency losses accumulated by your foreign stocks. Will you have the patience?

Source: Bloomberg

3. Hedging the currency risk of foreign stocks is expensive

As Yves Rebetez says in his article, the explicit costs (management fees) of ETFs with hedged currency risk are often reasonable. But there are hidden costs, such as those related to the intrinsic technical difficulties of hedging. These costs can be high, especially for stocks because of their higher volatility, and they can easily mean 1% to 1.50% less in foreign stock returns during bad times.2 In short, hedging the currency risk of foreign stocks protects your portfolio from losing cycles, but it may be expensive. There is no easy decision!

Conclusion

As Yogi Berra said, “It’s tough to make predictions, especially about the future.” How the Canadian dollar’s exchange rate will evolve is unpredictable. You need an effective strategy, regardless of the direction it will take. For foreign bonds, I believe you should not take any risks: hedge yourself! As for foreign stocks, I suggest using a strategy that many pension funds use: hedge half of the risk to reduce the impact and still control costs.

You can do this by distributing your foreign stock allocation between hedged and unhedged versions of the same portfolio. The table below mentions a few of these hedged or unhedged ETFs with which I feel comfortable.

Some Useful ETFs for Managing the Currency Risk of Foreign Investments

| NAME |

TICKER |

ASSET CLASS |

CURRENCY RISK |

| Vanguard U.S. Aggregate Bond Index ETF (CAD-hedged) |

VBU |

U.S. Bonds |

Hedged |

| Vanguard Global ex-U.S. Aggregate Bond Index ETF (CAD-hedged) |

VBG |

International Bonds |

Hedged |

| Vanguard U.S. Total Market Index ETF |

VUN |

U.S. Equity |

Unhedged |

| Vanguard U.S. Total Market Index ETF (CAD-hedged) |

VUS |

U.S. Equity |

Hedged |

| iShares Core MSCI EAFE IMI Index ETF |

XEF |

International Equity |

Unhedged |

| iShares Core MSCI EAFE IMI Index ETF (CAD-Hedged) |

XFH |

International Equity |

Hedged |

Source: PWL Capital, iShares, Vanguard Canada

—–

1 Y. Rebetez, Dollar canadien : se protéger ou non?, Les Affaires, August 26, 2017.

2 For more on this topic: R. Kerzérho, Currency-Hedged S&P 500 Funds: The Unsuspected Challenges, PWL Capital, 2010.